The Influence of Integrated Reporting on Management Control Systems: A Case Study

- Maria Serena Chiucchi

- Marco Montemari

- Marco Gatti

Abstract

The purpose of this paper is to investigate how Integrated Reporting can influence Management Control Systems (MCSs). To this aim, the paper presents a case study of a company which designed and implemented an Integrated Report (IR) that was used as a tool for communicating the company performance to the entrepreneur and as a tool for enriching the company MCS to visualize and measure the overall company performance. The case analysis shows that Integrated Reporting improves the measurement focus of the MCS thanks to the role played by the company’s Business Model (BM) throughout the IR development and to the process adopted to map the BM itself. The BM mapping process was highly iterative and allowed for a better understanding of the items affecting the value creation process and of their interconnections, thus directing the MCS to what really deserved to be measured. Strategic discussion around the BM also entailed an evolution of the control system, which became a strategic control system, able to support the discussion and the creation of new strategies. Moreover, the BM ensured a high level of integration and consistency between departmental reports and the company IR, on the one hand, and among the departmental reports themselves, on the other hand. In addition, the case analysis shows that financial indicators risk becoming “phagocytized” by non-financial ones and that the implementation process of the IR can lead to a heavier workload for the Management Control Department to provide for the non-financial aspects of performance. Finally, the case analysis shows that the Integrated Reporting visual representation and its underlying logic may not work if the tool is used for managerial decision making. While the guiding principles of Integrated Reporting were accepted by the company’s actors, the Integrated Reporting representation model based on the logic inputs-BM-outputs-outcomes was criticized as it was considered too complex and not able to represent the company’s integrated performance, reflecting instead a series of disconnected and disjointed individual performances. The critiques of this model were so sharp that they resulted in a change to its logic and the adoption of a different model, namely that of cause-and-effect relationships.

- Full Text:

PDF

PDF

- DOI:10.5539/ijbm.v13n7p19

This work is licensed under a Creative Commons Attribution 4.0 License.

This work is licensed under a Creative Commons Attribution 4.0 License.

- ISSN(Print): 1833-3850

- ISSN(Online): 1833-8119

- Started: 2006

- Frequency: bimonthly

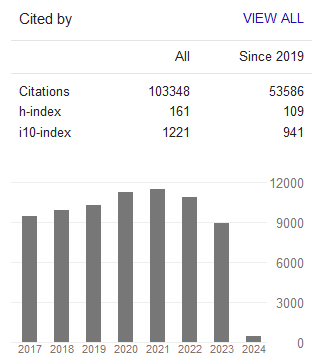

Journal Metrics

Google-based Impact Factor (2023): 0.86

h-index(2023): 152

i10-index(2023): 1168

Index

- Academic Journals Database

- AIDEA list (Italian Academy of Business Administration)

- ANVUR (Italian National Agency for the Evaluation of Universities and Research Institutes)

- Berkeley Library

- CNKI Scholar

- COPAC

- EBSCOhost

- Electronic Journals Library

- Elektronische Zeitschriftenbibliothek (EZB)

- EuroPub Database

- Excellence in Research for Australia (ERA)

- Genamics JournalSeek

- GETIT@YALE (Yale University Library)

- IBZ Online

- JournalTOCs

- Library and Archives Canada

- LOCKSS

- MIAR

- National Library of Australia

- Norwegian Centre for Research Data (NSD)

- PKP Open Archives Harvester

- Publons

- Qualis/CAPES

- RePEc

- ROAD

- Scilit

- SHERPA/RoMEO

- Standard Periodical Directory

- Universe Digital Library

- UoS Library

- WorldCat

- ZBW-German National Library of Economics

Contact

- Stephen LeeEditorial Assistant

- ijbm@ccsenet.org